Buying an Insurance Agency End-to-End Guide: Find, Derisk, Buy, Merge, Integrate

Szymon Zak

April 16, 2025

Strategy First: Why Acquire an Agency

Acquisition demands substantial capital, time, and opportunity cost. Without clear strategic objectives, you risk pursuing growth that doesn’t strengthen your market position.

The worst acquisition is one that achieves exactly what you aimed for when your aims were wrong from the start.

Geographic Expansion

Market saturation drives buyers to expand into adjacent territories. Focus on areas where you understand the market dynamics and competitive landscape. Avoid the common mistake of expanding into unfamiliar regions where you lack established carrier relationships or market knowledge. The most successful geographic expansions build from strength rather than leaping into entirely unknown markets.

Economies of Scale

Agency overhead typically consumes 30-40% of revenue regardless of size. Acquisitions let you spread these costs across a larger commission base. Each additional dollar of revenue contributes more to your bottom line than the last – provided you maintain operational discipline during integration. Many acquirers destroy value by failing to actually realize these economies after closing.

Carrier Relationship Enhancement

Strategic acquisitions can help you reach commission volume thresholds that unlock higher compensation tiers. Target agencies with strong carrier performance that complements your existing relationships. Before beginning your search, map your current carrier compensation agreements to identify specific premium volume targets that would trigger bracket improvements.

Access to New Markets

Acquisition provides immediate entry into specialized niches like cyber liability, professional services, or specific industry verticals. Target agencies with established expertise rather than trying to build specialized knowledge from scratch. The premium for specialized expertise is justified by the years it would take to develop comparable capabilities organically.

Talent Acquisition

In markets facing producer shortages, acquiring an agency may represent the most efficient path to adding experienced sales talent. Evaluate the quality and retention potential of the sales force as rigorously as you evaluate the book of business. The real asset often walks in and out of the building each day.

Competition Culling

Acquiring a direct competitor can reduce pricing pressure in your market while adding market share. This strategic objective works best in well-defined geographic markets where competitive dynamics are clear. The value lies not just in the acquired revenue but in the pricing power gained in the broader market.

Each of these objectives creates different criteria for target selection. The right acquisition for geographic expansion may not be optimal for carrier enhancement. Define your priorities before beginning the search.

Phase 1: Finding the Right Agency to Buy

The gap between available agencies and interested buyers means you need a systematic approach to identify viable candidates before your competitors do.

The best acquisition opportunities never make it to market. They’re created through relationships developed long before a sale was contemplated.

Creating a Target Profile

Develop specific criteria based on your strategic objectives. Revenue size range, geographic location, and lines of business specialization matter – but so do carrier appointments, staff composition, and technology platforms.

The more specific your criteria, the more effective your search will be.

Target Sourcing Channels

Finding good agencies requires some diversification, consider the below approaches.

Direct outreach to owners nearing retirement age often yields the best results. Network with insurance carriers and wholesalers who know which agencies might be considering a sale.

Engage with specialized M&A intermediaries, but recognize they represent sellers and will show the same opportunity to multiple buyers.

According to our larger P&C broker clients and founder’s network we established that between 3-5% of deals are effectively coming from seller-side intermediaries. The overwhelming majority of transactions are relationship-based.

Join agency networks and attend industry events where private conversations often reveal consideration of sale. Leverage professional associations like Big “I” that offer acquisition marketplaces. Monitor agency consolidation platforms that connect buyers and sellers directly.

Preliminary Screening

Once you identify potential targets, conduct initial qualification. Age of principal owners and succession options provide insights into potential timing. Growth trajectory over past 3-5 years reveals momentum and market position. Staff size and structure indicate operational complexity. Carrier overlap with your existing appointments may reveal simplicity or challenges in integration.

Technology compatibility determines how complex your integration will be. Geographic fit with existing operations impacts management oversight. Then initial valuation expectations set boundaries for financial viability.

The Initial Meeting

The first conversation sets the tone for the entire transaction. Focus on building rapport rather than negotiating. Explore the owner’s personal timeline and post-sale plans. Understand growth history and future projections. Learn about staff structure and key personnel. Ask about client retention rates and concentration.

Carrier relationships and loss ratios reveal hidden strengths or weaknesses. Back-office operations and technology determine integration complexity. Cultural aspects of the business predict post-acquisition challenges.

This initial meeting should evaluate both financial compatibility and cultural fit. Many successful acquisitions stem from relationships developed over months or years before formal negotiations begin.

Phase 2: Derisking the Acquisition with Due Diligence

Due diligence represents your best opportunity to identify problems before they become yours. Many insurance agency acquisitions fail to meet buyer expectations, often due to inadequate investigation during due diligence.

The money you save by rushing due diligence will keep you awake for weeks after closing.

Financial Verification

Look beyond the income statement to understand the business. Understand the business fundamentals like any investor should.

- Verify

commission statementsagainstcarrier reports. - Analyze

client retention trendsbyline of business. - Identify

revenue concentrationin key accounts. - Examine

contingent commission history. - Review

expense allocationsfor owner perks.

Assess normalized EBITDA with owner compensation adjustments. Verify trust account compliance and reconciliation. The goal isn’t just to confirm numbers but to understand how the business actually makes money – and where risk might hide.

Client Base Assessment

The value lies in the clients, not the entity.

The stability and growth potential of the client base will determine whether your investment thesis succeeds or fails. Look beyond current revenue to understand lifetime value and vulnerability.

- Review

retention ratesbyline of business. - Analyze client demographics and

potential attrition risks. - Evaluate client concentration and

dependency risks. - Review service models and client satisfaction metrics.

- Assess

cross-selling potentialwithin the book. - Identify

at-risk accountsdue to producer relationships.

Producer and Staff Evaluation

People often represent both the greatest asset and risk.

Again, remember that in most agencies, the real value walks out the door each evening. Your ability to retain key personnel will determine whether you realize the expected value from your acquisition.

- Review

producer employment agreementsandnon-competes. - Assess

producer compensationrelative to market rates. - Evaluate producer

ownership of expirationsorbook equity. - Analyze

staff turnover historyandretention risks. - Identify key personnel beyond producers.

Carrier Relationship Review

Carrier appointments rarely transfer automatically.

Many buyers discover too late that key carrier relationships come with conditions that weren’t disclosed. Direct conversation with underwriting leaders – not just marketing representatives – is essential to understanding the real state of these relationships.

- Verify

appointment transferabilitywith each carrier. - Review

loss ratiosandpremium volumeby carrier. - Identify any

at-risk appointmentsorconditional relationships. - Assess carrier

contract termination provisions. - Review

contingent commission agreements. Evaluate marketaccess for specialized risks.

Technology and Operations Analysis

System integration represents a major post-acquisition challenge.

The cost and complexity of technology integration often exceed expectations. Budget time and resources accordingly, especially if system conversion will be required (we will discuss that towards the end in Phase 5).

- Assess

Agency Management System compatibility. - Evaluate

data qualityand completeness. - Review

document management practices. - Identify

potential integration obstacles. - Evaluate

E&O claims historyand risk management. - Assess

policy checkingandquality controlprocesses.

Legal and Regulatory Review

We need to be transparent: insurance regulatory requirements vary dramatically by state and situation. This article cannot provide comprehensive legal guidance for your specific transaction.

Insurance agencies operate under complex, state-specific regulatory frameworks that create substantial compliance requirements during ownership changes. At minimum you may want to look into these issues:

- Agency and producer licensing

- Carrier appointment transfers

- Trust account management

- E&O coverage requirements

- Regulatory and carrier-side investigations

Many regulatory missteps cannot be corrected retroactively, creating permanent liability exposure.

Engage qualified legal counsel with insurance regulatory expertise early in your acquisition process. The right attorney will map state-specific requirements, identify potential compliance issues, and develop a transfer plan that maintains operational continuity while satisfying regulatory obligations.

Thorough due diligence typically requires 60-90 days. The investment in proper legal guidance prevents costly surprises after closing.

Phase 3: Structuring the Deal

Deal structure impacts everything from tax consequences to risk allocation. Most insurance agency acquisitions use one of several common structures, each with unique implications.

The structure of the deal often matters more than the headline price. The best price on the wrong terms leads to regret for both parties.

Asset Purchase vs. Stock Purchase

Asset purchases allow buyers to select specific assets and liabilities. Stock purchases transfer all assets and liabilities, including unknown ones.

- Asset purchases typically create more favorable

tax treatment for buyers. - Stock purchases usually create more favorable

tax treatment for sellers. - Asset purchases require individual carrier consent for appointments

- Stock purchases may preserve existing carrier appointments.

The choice between structures requires weighing tax, operational, and risk considerations unique to each transaction.

Valuation Methods

Insurance agencies are generally valued using multiple approaches.

Remember Howard Marks’ words:

Good investing doesn’t come from buying good things, but from buying things well.

Please note that these are ballpark estimates – acquisition opportunities happen through your perspective on business value and desirable factors.

Valuations have trended upward in recent years, particularly for agencies with strong growth, high retention rates, and specialized expertise. Acquirers are willing to pay premium for agencies that show great organic growth dynamics.

Revenue multiple– typically 1.5x to 3.0x annual commission and fee income in today’s market) provides a quick reference point.EBITDA multiple(typically 6x to 10xadjusted EBITDAfor quality agencies in 2023-2024) offers a more sophisticated approach based on profitability.Book value plus premium(typically 1.5x to 3x book value) appeals to financially oriented buyers.Discounted cash flow analysis(less common but more sophisticated) incorporates growth expectations.

Valuation varies significantly based on factors like size, growth rate, profitability, retention, carrier relationships, and staff quality. Market conditions also impact multiples, with current valuations near historical highs.

Earnout Structures

Most transactions include performance-based components.

An earnout is a contractual provision where the seller receives additional payment based on the business achieving specific performance targets after closing. This approach bridges valuation gaps and aligns interests during transition.

Revenue retention earnouts(based on retaining specified revenue levels) protect against client attrition.Growth earnouts(providing additional payments for exceeding targets) align incentives for continued performance.Profit-based earnouts(tied to profitability of the acquired business) encourage operational efficiency.Client retention earnouts(based on specific client retention metrics) focus on preserving key relationships.

Well-designed earnouts protect buyers while giving sellers enough upside potential to still make them care. Poorly designed earnouts create disputes that poison post-closing relationships. The details matter tremendously.

The earnout's effectiveness depends on precise definitions of measurement periods, calculation methodologies, management authority, and dispute resolution processes. Ambiguity in these areas creates dangerous gaps that can undermine the acquisition’s long-term success.

Seller Financing

Seller notes remain common in agency transactions. Typical seller financing ranges from 20-40% of purchase price. Terms typically range from 3-7 years. Interest rates typically range from 4-8%. Subordination to bank financing is usually required. Security interests often include UCC filings on business assets.

Seller financing demonstrates confidence in the transferred business and aligns interests during transition. It also addresses the reality that full cash offers rarely materialize for smaller agencies.

Bank Financing

Specialized lenders have developed expertise in agency financing. Commercial banks with insurance expertise offer relationship-based lending.

SBA 7(a) and 504 loans provide favorable terms for qualifying transactions. Insurance-focused specialty lenders understand the unique aspects of agency valuation.

Then Private equity and family office financing enters the market for larger transactions.

Working with lenders who understand insurance agency dynamics saves time and increases certainty of closing. General commercial lenders often struggle to value insurance agencies appropriately.

Legal Documentation

Key transaction documents include:

letter of intent(outlining key terms),purchase agreement(defining the transaction structure),promissory notes(for seller financing)employment or consulting agreements(for transition)non-compete agreements(protecting the acquired business).lease assignmentornew lease agreements,carrier consent letters, andclient notification lettersround out the package.

Working with advisors experienced in insurance agency transactions helps navigate these complexities efficiently. The investment in proper legal documentation pays dividends when disagreements arise after closing.

Key Consideration: The Seller’s Perspective

Understanding the seller's motivations helps you structure a compelling offer and navigate negotiations effectively.

The seller who accepts the highest price isn’t always making the best decision for their future. The buyer who pays the highest price isn’t always getting the best value.

Beyond the Purchase Price

Many sellers care about factors beyond maximizing proceeds. Legacy preservation and reputation in the community often matter deeply. Staff retention and continued opportunities represent commitments to long-term employees. Client service continuity and relationship protection reflect obligations to customers who provided loyalty for years.

Personal transition and post-sale involvement shape the seller’s next chapter. Tax implications and structure of proceeds affect actual realized value. Timing and certainty of closing matter for personal planning. Recognizing these non-financial motivations helps structure deals that truly satisfy sellers.

Emotional Aspects of Selling

For many owners, selling represents the culmination of a lifetime’s work. Loss of identity and purpose after decades in the business creates anxiety. Concern about client and employee welfare reflects genuine attachments. Fear of community perception if the business changes weighs heavily, especially in smaller markets.

Anxiety about life after the sale affects decision-making. Family dynamics and expectations about succession create complex pressures. Acknowledging these emotional realities helps build trust during negotiations.

Remember, you need to navigate seller’s fears – and they may not be on the rational side. As much as they are selling themselves to you, you are selling yourself.

What Makes an Attractive Buyer

Building rapport and demonstrating cultural alignment may secure deals even against higher offers. At the very least, it may incentivize the seller not to close off and negotiate.

The most successful buyers recognize that sellers choose partners, not just prices.

- Position yourself as the preferred acquirer by demonstrating cultural compatibility and shared values.

- Show commitment to staff retention and development.

- Explain your vision for market presence and growth.

- Provide evidence of successful prior acquisitions.

- Demonstrate financial stability and closing capability.

- Offer a clear role for the seller during transition.

Common Seller Concerns

Successful acquisitions address both financial and emotional needs. The best buyers recognize that purchase price alone rarely determines which offer a seller accepts or where they decide to push further negotiations. You don’t want to be their Plan B.

Address these issues proactively!

Protection of long-term client relationships tops many sellers’ concerns. Continuity for loyal employees matters deeply. Maintaining community involvement and charitable activities preserves legacy. Integration of systems and operating procedures affects daily experience. Retention of the agency name and brand identity connects to pride of creation. Post-closing flexibility and involvement shapes the seller’s future.

Phase 4: Post-Acquisition Merger

The period immediately following closing determines whether your acquisition succeeds or fails. Significant value can be lost during the integration phase if the process lacks structure and diligent execution.

Integration isn’t the last mile of acquisition – it’s the marathon that begins after you cross the starting line of closing.

Day One Priorities

Critical actions immediately after closing include executing carrier notification and appointment transfers.

These first actions set the tone for the entire integration process. Their execution signals to employees, clients, and carriers whether the acquisition will succeed or struggle.

- Implement

producer and staff retention agreements. - Announce the acquisition to clients and the market.

- Secure all client data and policy information.

Address immediate operational continuity issues. Establish integration management and responsibility.

Client Communication Strategy

Client retention represents your primary financial risk.

The communication strategy should emphasize continuity rather than change. Clients care about service, not ownership structure. Your messaging should reflect that reality.

- Develop a tiered approach based on account size and complexity.

- Personalize communication for key accounts.

Highlight benefitsto clients rather than focusing on the transaction.- Introduce relationship managers and service teams.

- Address potential service changes proactively.

- Create frequent touchpoints during the transition period.

Staff Integration

People integration determines whether systems integration succeeds.

You need to convince people that the change will be positive. Line staff aren’t particularly familiar with the rationale behind M&A. They may hold various doubts about the future, they may misread an acquisition as an event followed by consequences.

Even if these are just perceptions, leaving them unaddressed will make you susceptible to staff career decisions based solely on perceptions.

- Conduct detailed role and responsibility mapping.

- Identify skill gaps and redundant positions.

- Develop

retention strategies for key personnel. - Address

compensation differencesand expectations. - Provide clear timelines for operational changes.

- Establish

performance expectationsand metrics – but be lenient.

Be particularly attentive to cultural ambassadors – the informal leaders who shape opinion regardless of their position in the organization chart. Their buy-in often determines whether others follow.

Culture Alignment

Cultural integration takes 12-24 months and requires emotional intelligence, not just rational directives.

Cultural differences sink more acquisitions than any other factor.

- Create forums for addressing integration issues.

- Demonstrate desired behaviors yourself

- Accept reasonable resistance as part of the process.

- Assess

cultural compatibilitybefore closing. - Identify specific behavioral and operational differences.

- While your culture will typically prevail, incorporate positive elements from the acquired organization rather than imposing wholesale change.

You cannot demand people to change. It’s not a matter of rationally stating facts and expectations but rather managing emotions while accepting reasonable resistance.

Your goal here is not to build perceptions of a sudden revolution, or even worse beginning of tyranny. People dislike change, because it inherently doesn’t feel safe. Big changes introduce pressure and confusion – navigate that.

Operations Consolidation

Try to adapt the 80/20 rule during integration – focus on the 20% of changes that deliver 80% of the value, and defer less critical changes until the organization stabilizes.

Operational decisions drive both efficiency and experience.

- Identify quick wins for process improvement.

- Address obvious

redundancieswhile maintaining service levels. - Implement standardized procedures incrementally.

- Provide adequate training before requiring new approaches.

- Monitor service metrics closely during transition. Capture promised cost synergies methodically.

Knowledge Retention Strategies

The value of an acquired agency resides largely in relationships and tacit knowledge that doesn’t appear on any balance sheet.

The most valuable assets in an agency acquisition are the things you can’t see on any financial statement.

Structured Transition Plans

Without structured approaches, critical knowledge slips away as personnel adjust to new realities. Document what matters while the information remains accessible.

- Design formal knowledge transfer mechanisms.

- Create a detailed transition timeline with specific objectives.

- Pair key personnel from both organizations for knowledge transfer.

- Document critical

client relationshipsand preferences. - Map

carrier relationship ownersandkey contacts. - Inventory

specialized knowledge areasand expertise. - Establish formal

transition meetingsandcheckpoints.

Client Relationship Knowledge

The depth of client relationship knowledge often distinguishes exceptional agencies from average ones. This intangible asset walks out the door with departing personnel unless deliberately preserved.

- Preserve critical client insights by documenting key

contact preferencesand communication patterns. - Map

decision-makers and influencerswithin client organizations. - Capture

renewal strategiesand pricing history. - Document

known exposuresandcoverage challenges. - Transfer personal relationship information and history.

- Record client service expectations and

special arrangements.

Learning Deep Operational Knowledge

Capture how the business actually runs, not just how it’s supposed to run.

- Document

workflows and process exceptions. - Identify

undocumented workaroundsandsolutions. - Map

informal roles and responsibilities. - Capture

vendor relationshipsandperformance history. - Document

local market practices and expectations. - Transfer

technology customizations and configurationswhen applicable.

Every agency develops unique operational approaches that don’t appear in formal documentation. These tacit practices often contain significant value – or significant risk if not understood.

Carrier Relationship Knowledge

Carrier relationships built over decades can deteriorate in months without proper knowledge transfer. The personal element of these connections requires deliberate preservation.

- Preserve

carrier connectionsand insights by documentingunderwriter relationships and preferences. - Map

program accessandspecial arrangements. - Capture

submission strategiesandsuccessful approaches. - Transfer

loss controlandclaims handling processes. - Document

contingent commission structuresand history. - Preserve market intelligence about appetite and direction.

Knowledge transfer represents the most frequently overlooked aspect of agency acquisition; yet it often determines whether you realize the full value of your investment.

Phase 5: Data Migration and System Integration

System integration challenges delay your time to value from insurance agency acquisitions and contribute to client attrition during transition. Data migration requires specialized planning and execution.

The data migration process is where the promises made during acquisition meet the reality of day-to-day operations.

Why Data Migration Impacts Business Performance

At its core, an insurance agency's value is represented in its Agency Management System (AMS). This system houses every client relationship, policy detail, and carrier connection. When you acquire an agency, transferring this information correctly and mapping records appearing under different names to your own set of records (e.g. companies) preserves the value you purchased.

The business impact of data migration shows up in concrete ways:

Client service continuity depends on service staff having immediate access to accurate policy details. When information transfers incorrectly or incompletely, service quality suffers during the critical post-acquisition period when clients are already concerned about changes.

Revenue protection requires maintaining renewal dates, cross-sell indicators, and producer assignments. Missing or incorrect data leads directly to missed sales opportunities.

Operational efficiency suffers when staff must hunt for information across multiple systems or manually recreate missing data. This diverts attention from client service and revenue generation during the crucial integration period.

The Unexpected Complexity of Insurance Data

Insurance data involves more than simply moving records from one AMS to another. It requires preserving a complex web of relationships while resolving three fundamental differences:

- How systems from different vendors organize information (e.g. Applied Epic vs. AMS360) – this comes down to

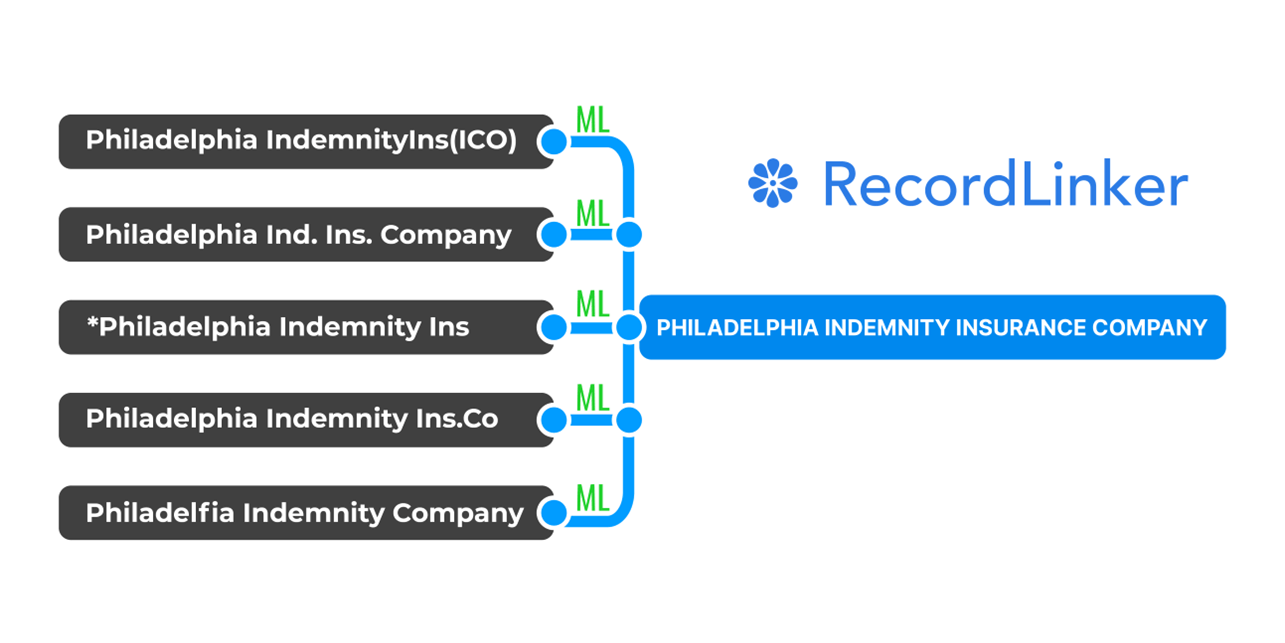

data formats and structures. For example, Applied Epic uses aflat company treewhile AMS360 usesparent-child hierarchies. - How naming standards differ – you need to map company A from the acquired system to company B in your AMS. You need to explicitly instruct your system that

'Philly Ind. Ins. Co.'means'Philadelphia Indemnity Insurance Company'. - Operational quirks about data – sometimes agencies will use records e.g.

brokersandbilling companiesdifferently. What’s a broker for you may not exactly overlap with what broker meant for the acquired agency’s data team. There could be some surprising rules on how commission splits happen between assigned employees, and so on.

Consider a typical commercial policy. It can connect to:

- A client record with multiple contacts

- A carrier with specific underwriting requirements

- Coverage types with detailed classifications

- Documents stored in various formats

- Service and sales staff with assigned responsibilities

- Commission structures with special arrangements

The challenge multiplies because different systems store this information using different structures, naming conventions, and relationship models.

Even within a single AMS there could be multiple Travelers companies appearing under 4 various names. Then these differences will surface from acquisition to acquisition. People are really creative in how they name things.

The Broken AMS Migration Process

Most brokers approach data migration through a process that hasn’t changed significantly in decades. It’s utter data labor.

First, technical teams extract data from the source system, this often involves your system’s vendor, data access clearance process, and a full database backup restoration.

During that time your data conversion team cannot map even a single company. This stage alone often takes 8 weeks, creating a roadblock for your data conversion.

Finally, data conversion analysts manually map entities between systems. For example, they match 'Philadelphia Ind.' in the source system to 'Philadelphia Indemnity Ins. Co.' in the destination system. They build these mapping tables for vital entity types – companies, coverages, lines of business etc. At that moment, they are most likely working under a tight deadline.

After mapping, they run test conversions to identify problems. Finally, they execute the full migration, move to post-conversion validation, and correct inevitable mapping errors.

This approach somewhat works, but it’s not scalable for larger agency buyers, and it places an enormous burden on data conversion teams. They often work extended hours for weeks or months to complete the mapping process, with workdays regularly extending into evenings and weekends during critical phases.

Transforming the Flawed Process

Modern solutions now address these fundamental challenges. Our platform, RecordLinker, represents one such approach that transforms the conventional migration process.

Given the length of the article, we will only touch upon this and send you to additional resources.

The end result is that you can ignore 8-week-long database backup restorations and get right into company mapping work from day 1. You can massively increase throughput of your migrations, and make sure your data people don’t burn out while barely seeing spreadsheets at 2 a.m.

By the way, it will take ~5 minutes to set it up – zero lengthy, heavy integrations.

Sounds promising? Visit these resources to learn more:

- [Blog] Insurance Agency Acquisitions – AMS Data Migration

- [Solutions] Data Conversion to Applied Epic

- [Solutions] Data Conversion to AMS360

- [Blog] Simple Data Analytics for Insurance Brokers

- [Podcast] Hidden Heroes of Insurance Data

Now, let’s start summing things up.

Making AMS Data Migration Strategic

The most effective acquirers treat data migration as a strategic capability rather than a technical afterthought:

- Include data migration assessment in acquisition due diligence.

- Budget adequately for conversion resources and technologies.

- Start planning conversion during negotiation rather than after closing.

- Invest in specialized tools that make migrations consistent.

- Set proper expectations for migration timelines.

By approaching data migration strategically, you protect the value of your acquisition investment and improve the integration experience for staff and clients alike.

Don’t Forget: Measuring Acquisition Success

Effective acquirers establish clear metrics to track performance against acquisition objectives. Implement structured measurement practices.

Review these metrics monthly during the first year post-acquisition and quarterly thereafter. Establish accountability for results and create intervention plans when metrics fall below targets.

Financial Performance Tracking

Analyze actual versus projected performance for key metrics:

- Revenue retention by line of business

- Expense synergies achieved versus projected

- Producer performance against targets

- Cross-selling success into the acquired book

- Return on invested capital

Integration Milestones

Measure operational integration progress:

- Client retention rates by segment

- Staff retention and engagement

- Technology integration completion

- Process standardization implementation

- Knowledge transfer completion

Strategic Objective Achievement

Assess progress against your original strategic goals:

- Geographic expansion metrics

- Carrier relationship enhancements

- Specialized expertise acquisition

- Market share growth

Most importantly – use what you learn for future acquisitions!

Document lessons learned to improve future acquisition approaches. The most sophisticated acquirers create a continuous improvement cycle that makes each successive acquisition more effective than the last.

Suggested Reading About Data Mapping and Migrations

Check our recommended reading list with articles and pages discussing insurance’s problems. We want to help you understand why your data teams struggle, and what to do about it.

Taking care of your AMS data quality and post-M&A migrations is a process that requires a shift in thinking. Technology in P&C insurance can both fail and bring benefits – ultimately it’s about how that technology addresses the needs of the end-users and whether it contributes meaningfully to their work.

- Data Mapping Between Systems: Keys, Values, Relationships (with P&C Insurance Examples)

- Data Governance in P&C Insurance for Applied Epic and Vertafore’s AMS360

- Data Conversion Roles and Responsibilities in Insurance

- In-House, Outsourcing, and Tech in Data Conversion

- Machine Learning in Entity Resolution with Industry Examples

To learn more about how RecordLinker can help you improve the quality of your data, request a free demo!