Digital Transformation in Insurance

Szymon Zak

July 10, 2024

Let’s go into definitions first. Stay with me – this is not about being a purist or getting online pats for being smart. How we understand the culture behind technology shapes how we use it and how we (fail to) benefit from it in business settings.

What Is NOT Digital Transformation?

Digitization does not cut it – think about just scanning documents to get their digital copies. Digitization is basically creating digital formats from originally analog data. This doesn’t eliminate paper. Does it change how your experts work with data? If they still need to do the same with just an added step, it’s not a transformation. Why do you need paper at all? Why do your employees need to still read information off paper or PDFs?

Digital transformation is not technology-first, because its goal is to change business processes. In order to change business, you need to understand how your processes work and what needs arise in your organization. It means that you should be purposeful about your tech choices.

Digital transformation is not about one-off projects or upgrades. Upgrading to a new software version is not transformative. Does it even change anything fundamental in how you run your business? True transformation involves a long-term commitment to re-evaluating and improving processes and systems.

It’s also not an emergency project for catching up with the industry’s bare minimum. You can’t think of change only when your tech and systems create too much friction, reveal horrendous effects of technological debt, or miss essential features. Instead, digital transformation implies foresight and proactivity.

Isolated efforts amidst lack of strategy and integration can’t be called a digital transformation. Digital transformation isn’t a collection of tactical, local initiatives as much as it isn’t a single upgrade,

It’s neither about exclusive focus on cost reduction. This is how business often thinks about all sorts of automation and solution choices. Remember that value is a different term from costs – and value can be created in various ways. So, it could be about quality of life, speed, employee retention, customer satisfaction etc.

Immediate costs savings, not incurring higher costs in the future, and rises in efficiency elsewhere in your company can be byproducts of digital transformation (because its goal is to improve processes and address needs). Beneficial change may not immediately be clear in terms of direct ROI.

Now, let’s sum it all up into a coherent definition.

What Is Digital Transformation Then?

Digital transformation is an organization-wide endeavor of meaningfully changing operations, specific business processes, products and services through technology and digital solutions.

Digital transformation relies on a culture oriented at striving to deliver exceptional value to customers. It’s a business commitment to constant digital innovation and improvement.

As a result of digital transformation and gaining the ability to deliver exceptional value to customers, businesses build a competitive advantage.

Why Digital Transformation Matters in Insurance

In the insurance industry, digital transformation is fundamentally about improving the customer experience and delivering more value. It’s not just about internal efficiencies; it’s about reimagining how insurance can better serve and protect clients in a rapidly changing world.

When we look at digital transformation with a strong client focus, we can easily come up with goals like: seamless client experience, personalized coverage, rapid claims resolution, proactive communication, value-added services and fostering loyalty, transparent pricing, as well as security and trust.

Digital Transformation vs. Insurtech

Digital transformation and insurtech are closely related but separate concepts in the insurance industry.

Insurtech refers to the use of technology innovations designed to squeeze out savings and efficiency from the current insurance industry model. These innovations often come from tech startups that are challenging traditional insurance practices. Examples include using AI for underwriting, IoT devices for usage-based insurance, ML for automating AMS data conversion projects.

While insurtech plays a crucial role in driving innovation, digital transformation involves reimagining business processes and customer experiences. Insurtech solutions can be part of this transformation.

The key difference lies in the scope and depth of change. Adopting an insurtech solution might improve a specific process, but digital transformation (progressively) changes how the entire organization operates and delivers value to customers. It’s about creating a digital-first mindset throughout the company, not just in isolated pockets.

Example Areas of Opportunity for DT in Insurance

Let’s take explore where digital transformation could apply in the insurance industry, including various levels of companies from carriers through wholesalers to brokers and agencies.

Common Industry Challenges

Every part of the insurance industry faces similar problems:

- Data migration and system conversion – struggling to move data from old systems to new ones without loss or corruption, problems with matching acquired data file structures between different software vendors.

- Mobile-first thinking – largely missing mobile experience that could enable clients to use self-service options, manage policies, report claims, and get support on-the-go. More than 50% of web traffic comes from mobile!

- Unused customer data – failing to leverage collected data for personalized services or pricing.

- User adoption – getting staff to fully embrace and utilize new digital tools.

- Data security – everyone handles sensitive customer info and protecting it is crucial.

- Regulatory compliance – insurance is heavily regulated. Keeping up with changing rules affects all players.

- Customer experience – the push for better, faster service impacts the whole industry, from quotes and underwriting to claims.

- Technology integration – connecting different systems and ensuring they work together smoothly is a universal challenge.

- Talent acquisition – finding and keeping skilled tech workers is tough for the entire industry.

- AI and automation adoption – everyone in insurance is trying to figure out how to use AI effectively.

Insurance Carriers: Transforming the Core

Carriers form the foundation of the insurance industry, and their transformation ripples through the entire ecosystem. Their digital journey focuses on modernizing core operations while enhancing customer value.

- Underwriting failures – relying too heavily on outdated risk models, limited number of data sources, underused new and relevant data sources, leading to poor pricing and increased losses.

- Claims leakage – inefficient processes causing overpayments or unnecessary legal expenses.

- Product development lag – slow creation of new offerings for emerging risks (e.g., cyber insurance), risking losing market share.

- Legacy core systems – many struggle with outdated policy administration, billing, and claims systems that can’t handle modern data needs or integrations.

- Data silos – different departments use separate systems, preventing a holistic view of customers or risks.

- Telematics integration – difficulty in processing and utilizing real-time data from IoT devices for usage-based insurance.

Wholesalers: Bridging Strategic Gaps in Insurance Supply Chain

Wholesalers play a crucial role in connecting carriers with brokers, especially for complex or niche risks. Their digital transformation efforts aim to streamline these connections and add value to both sides of the equation.

- Capacity mismanagement – inability to quickly adjust to changes in carrier appetites, missing placement opportunities.

- Specialty market blind spots – failing to identify or access niche markets for hard-to-place risks, lack of market analytics tools.

- Broker relationship breakdown – poor communication or slow response times damaging key partnerships.

- Program business stagnation – failing to innovate or expand successful insurance programs.

- Digital collaboration platforms & API connectivity – difficulty in creating secure, efficient platforms for real-time collaboration with brokers and carriers.

- Automated submissions – challenges in creating systems that can automatically route and underwrite submissions based on carrier appetites.

The Unseen Data Heroes of Insurance – Listen to Our Guest Episode

Our founder, Roman Stepanenko, shares insights into challenges of data administrators and data conversion teams in insurance.

Discover the gaps in the process, and the reality of manual workflows of insurance's data people. They are some of the most hard-working and unnoticed 'silent teams'.

Data conversion analysts, business systems analysts, implementation specialists, and data admins keep large brokers going after agency acquisitions.

Insurance Brokers: Keeping Client Relationships Strong

Brokers are the face of insurance for many clients, making their digital transformation particularly impactful on customer experience. Their focus is on leveraging technology to provide more personalized, efficient service.

- Post-M&A integration and AMS consolidation for records from acquired agencies – this process is slow and largely manual.

- Risk assessment shortfalls – inadequate analysis leading to coverage gaps for clients.

- Commission-driven mindset – prioritizing high-commission products over client needs, resulting with higher margins at the expense of revenue and scale

- Business-wide, accurate, analytics – data analytics implementation doesn’t have to be daunting, and for bigger organizations should look into linking disparate data sources for reliable BI insights.

- Renewal complacency – lack of proactive policy reviews, risking client loss to competitors.

- AMS limitations – many AMS systems lack advanced features like predictive analytics or integrated marketing tools.

- Client portal development – challenges in creating user-friendly portals that provide real-time policy information and self-service options.

- CRM integration – difficulty in fully integrating CRM systems with AMS for a complete view of client interactions.

Agencies: Going Beyond Local and Small with Insurance

Insurance agencies, often serving specific communities, face unique challenges and opportunities in digital transformation. Their efforts center on maintaining their personal touch while embracing the efficiencies of digital tools.

- AMS selection and implementation – smaller agencies often struggle to choose and properly implement the right AMS for their needs, many problems with processes start from here.

- Multi-carrier quoting – over-reliance on a single carrier, difficulty in setting up systems that can quickly generate quotes from multiple carriers.

- Local market fixation – missing broader market trends or emerging risks relevant to their client base.

- Technology adoption paralysis – hesitating to invest in necessary tech, falling behind more agile competitors.

- Document management – challenges in transitioning from paper-based to fully digital document systems.

- Producer performance tracking – lack of good tools to track and analyze individual producer performance and guide improvements.

Approaching Digital Transformation in Insurance

Planning and executing digital transformation in insurance requires a strategic, holistic approach.

1. Choose the Bottom-Up Approach

While leadership support is crucial, successful digital transformation should start from the ground up. Employees who work directly with customers and handle day-to-day operations often have the best insights into what needs to change.

You don’t need a rooster of consultants and overly-seriously-sounding digital maturity assessments to start making meaningful change.

Embrace open communication to let your employees understand the purpose behind changes and new direction. If digital transformation happens against employees or without engaging them you risk great confusion and pushback.

Encourage open feedback to create a culture where employees feel safe providing honest feedback, even if it’s critical. This openness can uncover pain points and opportunities that might be invisible from the top.

Break down silos between departments. Digital transformation affects the entire organization, so it requires collaboration across all areas.

2. Keep DT Business and Client-Focused

Start with problem-solving and business needs instead of starting with technology, begin by identifying the problems you’re trying to solve. This ensures that your digital transformation efforts are purposeful.

Map your processes to understand how they work and what needs or could be changed. This is a foundational thing to do for anything related to business process automation. It could help you spot where inefficiencies begin or where their results appear.

Set clear and relevant KPIs for your digital transformation efforts, and be prepared to adjust your strategy based on results. Don’t focus primarily on ROI, or at least think which operational metrics influence ROI, and any other indirect metrics relevant to the business process under transformation.

Embrace customer feedback by looking at client feedback with an open mind. Negative feedback, in particular, can highlight areas ripe for transformation. Use tools like Net Promoter Score (NPS), customer journey mapping, and NLP analysis to identify pain points.

3. Know What Innovation Means

Don’t try to transform everything at once. Start with pilot projects, learn from them, and scale successful initiatives. Iterative approach is your safest bet, because you can’t hope to change the culture overnight.

Create an environment open to trying new ideas. Accept that not all initiatives will succeed to encourage experimentation. Innovation needs freedom to fail, and your leaders will be more willing to take action without fearing repercussions.

Digital Transformation in Insurance Wrapped Up

Digital transformation, when done right, can revolutionize the client experience in insurance, making it more personalized, transparent, and valuable. It’s not just about adopting new technologies; it’s about fundamentally changing how insurance companies operate to better serve their clients.

Remember, digital transformation is not a one-time project but an ongoing journey. It requires a great shift in mindset across the organization, from leadership to front-line employees.

By taking a bottom-up approach, listening to employees and customers, and fostering a culture of continuous improvement, insurance companies can navigate the complexities of digital transformation and emerge stronger and more customer-centric.

As we move forward, successful insurers will be those who can create seamless, personalized experiences that truly meet their clients’ needs. They will use data and technology not just to improve internal processes, but to anticipate and solve client problems proactively.

Suggested Reading About Modern Data Management

Check our recommended reading list for practical insights and easy-to-understand resources to help you establish good data practices in your organization. Proper data management is not simple – learn foundational concepts to discover helpful solutions to your data challenges.

- Artificial Intelligence in Insurance: Applications and Honest Advice

- Homegrown Data Analytics for Insurance Brokers and Agencies

- Handling Data Migration Risks

- Normalizing Company and Vendor Names

- [Guide] Building Your Own Record Linkage Solution

- 5 Key Components of Master Data Management

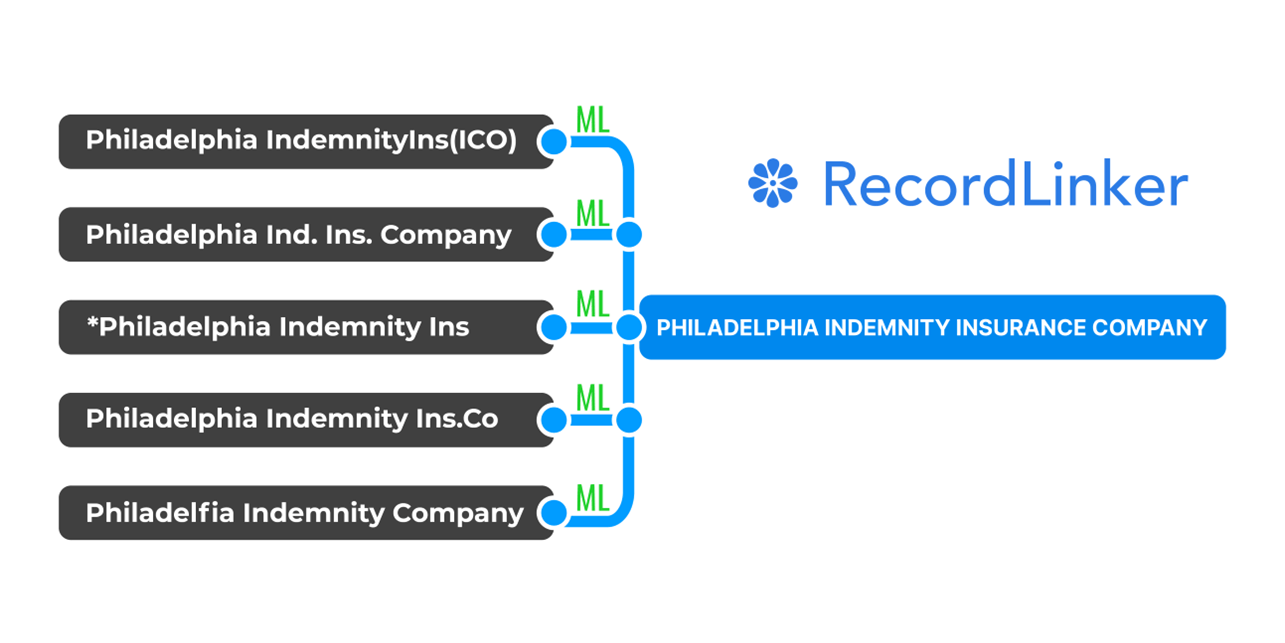

RecordLinker uses Machine Learning to make your data conversion painless. We easily handle conversion projects for systems like AMS360, Applied Epic, Sagitta, BenefitPoint, Guidewire, and more.

You can reliably cut conversion project times with ML from weeks to days.

Auto-map your records during system migrations (e.g. writing companies and parents), identify wildly different spelling variants as a single entity, bulk-create missing companies and configure employees in your core system. Standardize entire data marts.

To learn more about how RecordLinker can help you improve the quality of your data, request a free demo!